We present review of margining as Credit Counterparty Risk mitigation tool in OTC derivative trading based on International Swap and Derivative Association standards. Practical part of paper contain demonstration of impact of margining thresholds, amounts and timing parameters on portfolio exposure.

We just have published white paper about close-out netting in Credit Counterparty Risk.

The paper presents brief summary of netting principles and effects in Counterparty Credit Risk. We discuss advantages, types of netting and main concepts for institutions with derivative portfolios.

From the practical point of view, we first implement concept of netting with simple examples and then show netting effects for simulated portfolios of derivative transactions. In addition to collateral and margining, netting is one of main methods of CCR mitigation.

The full text of white paper is available at our Research Papers page. You can also download it by the link below:

On September 2nd, the Basel Committee and IOSCO released the final framework for margin requirements for non-centrally cleared derivatives.

According to the document, non-centrally cleared derivative trades will be subject to initial and variation margin, in order to mitigate the inherent counterparty risk. The framework has been designed to reduce systemic risks related to over-the-counter (OTC) derivatives markets, as well as to provide firms with appropriate incentives for central clearing while managing the overall liquidity impact of the requirements.

Compared with the near-final framework proposed earlier this year, the final document exempts some deal types from initial margin requirements (such as physically settled FX forwards and swaps). Also, it permits “one-time” re-hypothecation of initial margin collateral among the features to mitigate the liquidity impact associated with the requirements.

The implementation will be spanned over a four-year period, with a first milestone on 1st December 2015.

Our latest white paper provides practical guidelines on estimation of Exposure at Default, CCR default capital charge and standardized CVA capital charge, based on the methods proposed in Basel 2 and 3, and compares the capital charge imposed under different methods (Current Exposure Method, Standardized Method, Internal Model Method, and the recently proposed Non-Internal Model Method) and risk weighting approaches (Standardized and Internal Risk Based), using the calculations performed for a portfolio of derivatives in PrevioRisk software.

The results of practical implementation show that Internal Model Method of EAD estimation produces about a quarter (27-28%) lower CCR capital charge than Standardized and NIMM methods. Particularly, IMM allows to recognize fully the effect of netting and margining, and saves capital for trades influenced by market factors with low volatility. In addition, the results confirmed that IRB risk weighting approach results in lower required capital estimates than the Standardized one, with capital relief from IRB implementation reaching 35-40%.

The full text of white paper is available at our Research Papers page. You can also download it by the link below:

When a bank does not have regulatory approval to use Advanced CVA capital charge, which allows to calculate regulatory capital on counterparty-by-counterparty basis, the bank must calculate capital on portfolio level using the following formula (see Basel III: A global regulatory framework for more resilient banks and banking systems para. 103).

As was mentioned above, this is formula for Standardized CVA capital charge calculated at portfolio level, which in the given form does not allow to define main drivers and components of CVA capital charge. For this purpose we use decomposition, based on EAD on customer or even trade level. As we will see, it is possible to manage portfolio by hedging separate trades. Here is the example of CVA capital decomposition for portfolio of 250 derivatives with total notional of 4.5 bln (all numbers are in USD mln).

Double Strike Floor and Double Strike Cap (N-Floor and N-Cap) are modifications of the Interest Rate Floor/Cap. In a Knock-Out Floor/Cap, once the trigger rate is breached (Knock-Out or KO event), the protection of the Floor disappears for that period. In a Knock-In Floor/Cap, protection does not appear unless the trigger is breached (Knock-In or KI event). Here are examples of payoff profiles for Double Strike Floor and Cap.

Compono Strategia, a credit risk services provider, has leveraged risk analytics from RiskMetrics, an MSCI brand. These analytics will deliver an integrated framework for counterparty credit risk management through the PrevioRisk platform for banks, brokers and corporates in the Middle East.

Uzma Naeem Ikram, Director Compono Strategia, says: “Banks, corporates and financial institutions will benefit from the integration of PrevioRisk’s power in fully configurable rule and aggregation functionality, with the best-of-breed risk and stress testing capabilities provided by RiskMetrics Web Services. Sell-side traders and risk managers will benefit from the ability of PrevioRisk’s technology to support all margin models and asset types, with the flexibility to respond dynamically to client needs and market events. Clients will gain greater control and transparency from enhanced reporting though the replication of counterparty methodologies and seamless integration of analysis and data.”

Robert Ansari, Head of Coverage for the Middle East, MSCI, adds: “Given the forthcoming implementation of the Basel III guidelines, the risk measurement and management of bilateral and central counterparty (CCP) agreements has become a greater area of focus for our clients globally. RiskMetrics counterparty credit risk analytics are evolving to help our clients become more compliant with their internal and regulatory requirements. We are delighted that Compono Strategia has chosen to utilize our analytics, allowing PrevioRisk platform users to receive intraday risk and exposure analysis, which will then drive the generation of reports on-demand across multiple asset classes.”

Key benefits of the offering include: Counterparty Credit Exposure, CVA, client-specific stress scenario based margining; what-if-scenarios; combined risk and margin rule-based exposure analyses.

For further information on PrevioRisk, please visit their web site at www.previorisk.com

For further information on MSCI, please visit our web site at www.msci.com

There is a lot on misunderstanding in interpretation of risk and uncertainty. To understand the difference between these two terms begin by exploring what is meant by “risk”. In general, risk is the chance of injury, damage, or loss (Webster’s New World Dictionary).

Risk: We don’t know what will happen in future, but we do know the distribution of future outcomes. Uncertainty: We don’t know what will happen in future, and we don’t know what the possible outcome distribution is.

In other words, the future is always unknown — but that does not make it “uncertain.”

Although the definitions we have just provided are very simple, they can explain a lot when going into details.

The S&P 500 was up about 1 percent at about 1,578 at 1:07 p.m. New York time today when a posting on the Associated Press Twitter account said there had been explosions at the White House and President Barack Obama had been injured. The benchmark gauge for American stocks erased almost the entire gain, falling as low as 1,563.03 by 1:10 p.m.

One of the typical tasks when constructing stress-test scenario is risk factor selection. Obviously, each portfolio has trade-specific factors which directly influence present value (PV) and potential future exposure (PFE) of positions and, thus, overall risk exposure and performance of the portfolio. For example, credit default spreads are needed to price Credit Default Swaps.

In most cases, however, there are global macroeconomic factors (GDP, interest rates, oil price etc.) and market-specific time series (such as market indices and key market drivers), which have indirect influence on trade-specific factors and, thus, portfolio value. This relationship can be measured ether by correlation, if relationship has no lag, or by autocorrelation, in case of lagged effect.

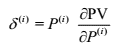

The delta equivalents of a position describe the response of a position/portfolio to a change in the market data.

Delta equivalent is the derivative of the Present Value with respect to a given risk factor, multiplied by the value (price) of that particular risk factor: (more…)

Marginal Expected Exposure (Marginal EE) represents the effect of each specific contract on aggregated Expected Exposure of the portfolio. This concept is useful for understanding which trades are contributing most to the total portfolio risk, as well as for assessing the return on a specific trade against its contribution to total exposure. If portfolio includes only one contract, then Marginal Exposure of this contract equals to portfolio exposure.

The goal is to find allocations of that reflect trade contribution to the overall risk for each period and sum up to the counterparty-level .

Please complete the form below to proceed with download

The information will only be used by Compono Startegia, and will not be disclosed to any third parties. For further details please refere to our Privacy Statement