Marginal Expected Exposure (Marginal EE) represents the effect of each specific contract on aggregated Expected Exposure of the portfolio. This concept is useful for understanding which trades are contributing most to the total portfolio risk, as well as for assessing the return on a specific trade against its contribution to total exposure. If portfolio includes only one contract, then Marginal Exposure of this contract equals to portfolio exposure.

The goal is to find allocations of that reflect

trade contribution to the overall risk for each period

and sum up to the counterparty-level

.

1. No netting

“No netting” here means that contracts are fully independent and we cannot net the value of separate trades. in this case equals to the sum of the individual components; hence, the

will equal the

.

If no netting is assumed, then Total Exposure of portfolio is just a sum of individual positive exposures. The logic is straightforward: Marginal Exposure for given contract at certain period of time is computed as average of positive simulated exposures for each specific contract. Now assume we have 1000 of simulations of exposures. Marginal exposure in this case should be computed as expected value across all simulations.

, where

is index function (taking the value 1 if underlying condition is satisfied, and 0 otherwise).

2. Netting

Similar formula can be applied for portfolio with netting:

,

where is index function (as defined above).

Difference with previous formula is the following: average is computed only across positive values if netting set

was positive. If netting is assumed, then Marginal Exposure for given contract at certain period of time is computed as the average of:

- positive simulated exposures, if total value of the set, to which this contract belongs, is positive;

- 0, if value of this contract in this simulation is zero or negative.

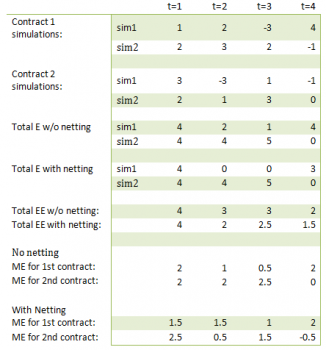

Example: 2 contracts, 2 simulations, 5 periods

For example, in the table above in the second period we compute ME for the first contract as (2*1(0>0)+3*1(4>0))/2=(0+3)/2=1.5

Please notice that the sum of marginal exposures across all contracts in the portfolio equals to total exposure.

Notations:

— contract index;

— simulation index;

— period index;

— simulated exposure for contract

at period

where

is number of simulation;

— expected exposure for contract

at period

;

— total exposure in simulation

at period

;

— total expected exposure at period

;

— marginal exposure for contract

at period

;

— number of simulations.